“Everybody has to feel like they have a safe place to work, and that they have a voice at work.” - Rich Jones

Credit unions and banks have been experiencing growing pains for the last decade or so. It’s time for them to make their products and services more available in an increasingly digital world. Now, one year into the COVID-19 pandemic, many of the financial institutions that pressed against the idea of “going digital” are realizing that it’s critically important to make their organization more accessible.

The key to making this happen?

Digital Strategy Driven by a Single Leader

For too long, banks and credit unions have been working in conflict from an internal perspective. Lending teams have their own digital initiative for online loan and mortgage applications. Individual branches take control of their own digital realm. IT does their own thing. And marketing is on its own course.

But now, there’s an opportunity for leaders to drive a singular, focused digital strategy as a unified organizational initiative.

“Our org charts need to kind of be reinvented. Org charts should follow strategy. Strategy should not follow org charts,” says Rich Jones, president and principal at Leading2Leadership.

For strategic initiatives to become more digitally friendly, there needs to be an executive to unite each of these silos to drive that initiative forward and share a common business plan to actually make it happen. This means that for many organizations, the idea of leadership has to change — it must be redefined.

For too long, leadership has been seen as the job of the chosen few — especially as dictated by org charts. But Rich disagrees with this idea.

Leadership isn't for the few; leadership is for the masses.

Leadership in a post-COVID, digital-first world should (and will) be vastly different than how it ever looked before. It used to be that leadership was all about the position and title — AKA managing a team of people.

But today, that whole concept has reached its expiration date. At every job within a financial brand, you’ll find experts in their roles, all of whom know a lot more about what they do than those overseeing them. This includes tellers, member service people, loan officers, underwriters — everyone on the team.

They are all experts at what they do.

Rich calls this a “distributed leadership model. He explains, “Because you're an expert, you have to have a voice in anything that impacts your ability to do this job well.”

To best serve the members and customers of a financial institution, each person on the team needs to be heard and believed. Rich continued, “And I think that's kind of missing right now in leadership development across credit units; it’s still kind of this top-down [approach] … We’ve got to turn the pyramid upside down.”

The first CEO that Rich ever worked for shared an interesting perspective with him about learning from those around him.

"The higher you get in the organization, the less what's going on on the front line."

Banks and credit unions must let the front line drive what is important. It’s not about the board or the senior vice president (SVP). Instead, it’s about engagements. It’s about what the frontline workers hear every day when they engage with the customer.

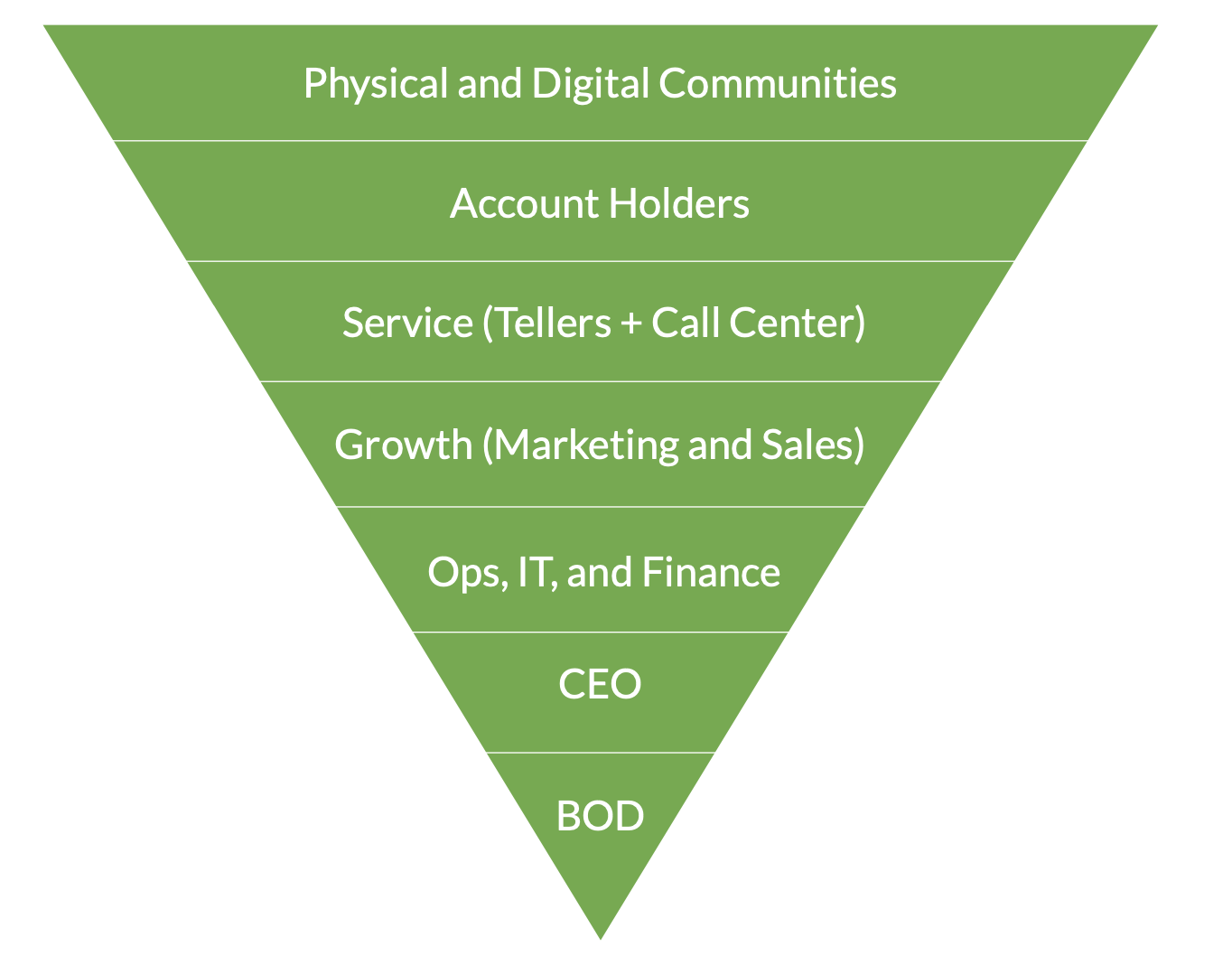

Flipping the Org Chart

How should community banks and credit unions lead? When it comes to the digital growth blueprint, they need to turn the organizational pyramid on its head.

At the top, it’s not SVPs — it’s the community. That’s ultimately the group the financial institution serves. They are the ones that lead initiatives. What follows are account holders and then the team members who are on the front lines. They are the ones that understand the ins and the outs of what community members want and need.

After all, the face of a community bank or credit union isn’t the board members. It’s the tellers. These are the people who engage with members every single time, who hear what customers are saying and what problems they're having.

But many organizations diminish the contributions of these team members right from the get-go. They're considered entry-level instead of experts.

Rich explained how now is the perfect time to change all this:

“One thing that COVID has done though, I think, that is a real plus for the whole industry is, we have established a new appreciation for what we consider to be essential employees ...That is the person that's having that conversation through now, a slice of plexiglass, but engaging people on a human level. The face of the credit union should never be diminished as an entry-level job. It should be considered a professional job that is giving real guidance and assistance to people at the point of contact. What better role is there?”

Today, tellers — those once considered to fill “entry-level roles” — are now on the front lines of this financial health crisis. No one is just a teller. They are financial advisors and guides. James Robert highlighted their unique position. "You know what? I do more than just transact with someone — I transform someone's life. And the way I do this is financially."

Empowering Team Members as True Experts

It doesn’t take much research to discover that many banks and credit unions share the same kinds of mission statements. They all revolved around helping their account holders “achieve financial success.”

Rich shared that what he realized is that when banks diminish the pivotal role that frontline workers play in this, nobody wins. If tellers don’t feel empowered to help their members, they can’t serve them the way they want or need to. Frontline tellers might feel uneasy at first giving advice to people who are looking to deposit $50,000, $100,000, or $200,000.

However, it’s time to flip this thinking on its head.

Rich elaborated. “Think about this a minute. You know more about what products and services you have available to them than they know. You are the expert here. You may not have the same balance sheet, but you have more knowledge than they have about what you can do for them."

It’s an entire paradigm shift that everyone within the institution needs to understand and embrace. Frontline workers should be empowered to see themselves as experts on the entire financial organization — not just transactional experts.

Culture’s Role in Digital Transformation

When it comes to digital growth and digital transformation, the role of organizational culture is paramount. Tellers, managers, member service representatives, SVPs? None of them have used the app or the website to do things like open an account or complete a transaction online because they’ve never had to do so.

Organizations must become completely digitally savvy when it comes to their banking products and services. This puts them in a better position to provide exceptional service. A culture that encourages this understanding is absolutely essential.

Rich shared, “You also move up the org chart, and you'll find that you've got executives that have never even used their mobile app before. How in the world can you have a digital strategy when people in the organization are totally unaware of what a cool tool this is?”

When the Digital Growth Institute begins work with a bank or credit union, it starts with diagnostic studies composed of key stakeholders like marketing, sales, and leadership teams. 30% to 40% of the time? These stakeholders hold primary accounts with other financial institutions! Plus? They’ve never applied for a loan or opened an account at their own financial brand. They have never experienced the culture for themselves.

Once these stakeholders go through that process, they can start to see where the gaps are and why it’s so important to foster a digitally-focused culture.

Rich mused, “It'd be a really fun exercise to sit in a room with 10 key people at different levels of the organization, everything from the frontline to the executive suite. And have them do an online loan application right there in the room on their computer, just like they were doing it from home. And what they're going to find out is how totally broken the process is.”

Creating for the Consumer

When integrating a new online banking application or a new mobile banking initiative, all too often, the people driving the conversation more than anyone else are the compliance and risk mitigation teams.

Of course, compliance and risk mitigation are incredibly necessary. But many times, they build in protections to address fears of abuse and fraud. The result? They include layer upon layer of risk mitigation and compliance on top of what should be a fairly simple operation. The application has not been engineered with the consumer in mind.

There must be consistency across the organization, regardless of what channel members enter through. The rules are the same. The risk mitigation is the same. The compliance is the same. Everything should be the same. But what happens all too often is that the online version is muddled, complicated, and nearly impossible to complete.

Banks must ask themselves, “At what point does compliance become a cost and detrimental to the experience?” “Where will there be an exponential drop-off in digital conversions?”

Too many warnings or gates will scare off or deter customers. James Robert put it plainly. “At what point does compliance become a cost?”

Of course, protections are certainly warranted. But the challenge facing credit unions today is crafting a friendly digital experience.

When Plans Are Disrupted

If there’s one thing financial institutions learned in 2020, is that plans don’t go the way we expect them to. Pandemics happen. The mortgage crash of 2008 happened. Things are bound to happen, and they will most certainly disrupt even the best-laid plans.

What has to happen? Banks must have a process in place to quickly understand the full impact of these disruptions, then determine how to rethink their plans to match a new future. When banks are thrown a curveball, some of their plans may be slowed down while others — like digital transformation amidst social distancing — must be expedited.

When plans get upended, the most important thing financial institutions can do is prioritize. Most often? The priorities will be the elements that can have the most member impact — what will most affect the relationship with members or the overall member experience. And if it doesn’t meet this requirement? It doesn’t mean these lesser priorities get eliminated. As Rich explained, “It may have to wait a year, or two years, or three years before it elevates up to where it has a chance of having the kind of impact organization needs.”

It’s about value creation — having the courage to have difficult conversations and ask tough questions.

And ultimately? It’s about accountability.

Right now, the top priority for financial brands moving towards the end of the COVID-19 era is refining the digital experience. But just as important is something that Rich shared about creating a company-wide culture of leaders.

“We have got to figure out how to make our workplaces safe for everybody. I don't care what race, religion, color, orientation. Everybody has to feel like they have a safe place at work and that they have a voice at work.”

He continued, “Because if it works for them, it's going to work for the member.”

This article was originally published on April 20, 2021. All content © 2024 by Digital Growth Institute and may not be reproduced by any means without permission.